5 Retirement Roadblocks: How Life Insurance Can Help - A.I.D.

A.I.D.

May 7, 2019

5 Retirement Roadblocks: how Life Insurance Can Help

The best laid plan requires a hedge. And this certainly applies to retirement planning. Even if clients are saving enough for retirement, there remain 5 roadblocks to a well-intentioned retirement plan that need to be addressed:

Rising Healthcare Costs. Healthcare will likely represent the largest expense during retirement. The estimated out-of-pocket medical costs for a couple age 65 today over their retirement is approximately $280,000, according to the Fidelity’s 2018 Study on Retiree Health Care Cost estimate. The same Fidelity study estimated the cost to be $260,000 in 2016, illustrating the magnitude of the annual escalation in costs. Medical inflation will increase this amount even further. Consider that the general rate of inflation is 1%, while the medical costs inflation rate is running at more than double that rate, or 2.49% annually. Consider, too, that the purchasing power of a dollar can decline over the years. It becomes harder to maintain a lifestyle when income doesn’t increase. For example, a look at a retiree’s expenses back in 1989 reveals that the buying power of a dollar as of 2015 had been cut to almost half.

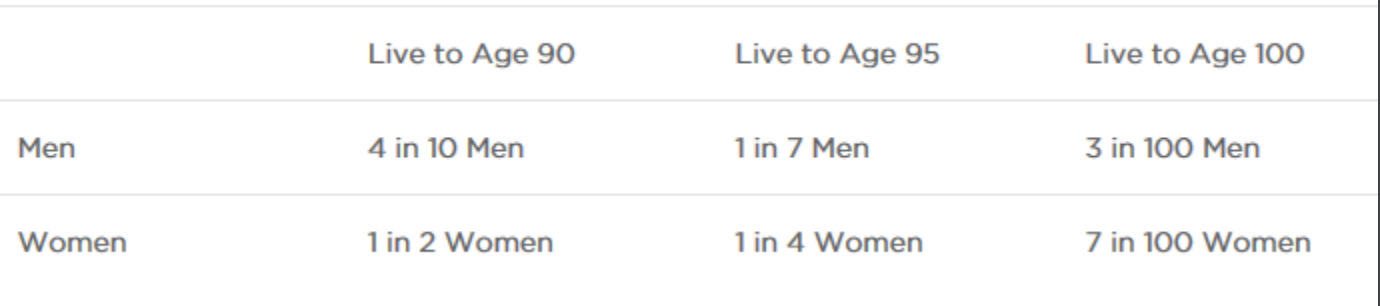

Living Too Long. A chronic or terminal illness can cost thousands of dollars each year. It’s tough to predict what those costs will be or when a client will begin to incur them. However, taking into account their family history, clients can get an idea of what may happen—though this certainly is not a given. Chronic diseases like cancer, heart disease or diabetes are caused by a combination of factors that include genes, behavior, lifestyle and the environment. It helps to know what the risks are and how to mitigate the risks– and the costs– when you are fortunate enough to live longer than expected. What are the chances you will become chronically ill and require long-term care? Take a look at statistics on longevity alone:

Based on 2015 Basic Valuation table, Nonsmoker, Select & Ultimate mortality rates. American Academy of Actuaries and Society of Actuaries.

The key question a client must answer, then, is “How long will I live?’ In other words, retirement can last for more than 30 years, even with a chronic illness. Will sources of funding be there, especially if there are unexpected expenses that arise? Consider the following unexpected expenses:

Change in tax code

A natural disaster

Care over an extended period

Significant financial help adult children may need from parents.

Market Volatility. If the stock market has a downturn while the client is taking income, this downturn will have a dramatic impact on the amount of time money will last. Having sources of income to tap that are not tied to the market will help to preserve principal during market dips.

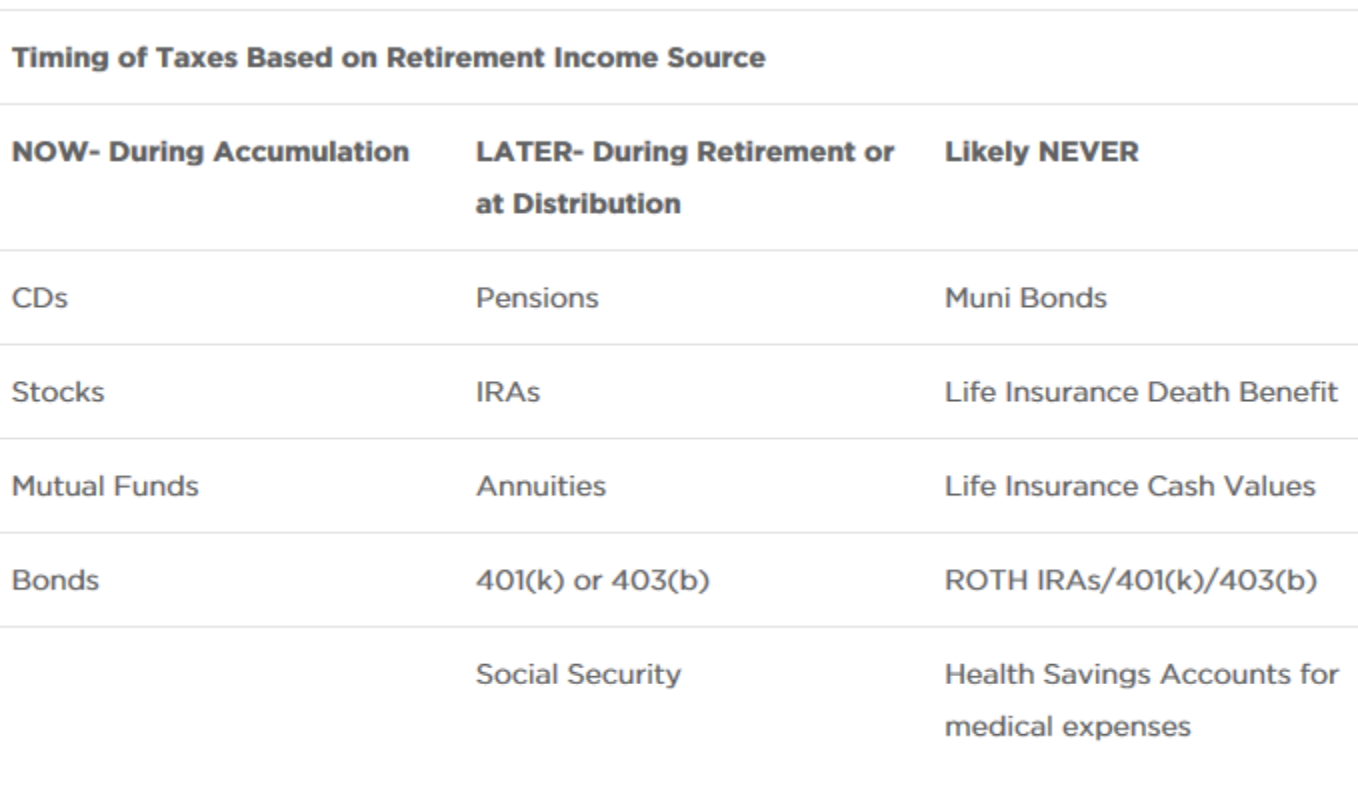

Taxes. Taxes will most certainly reduce income in retirement. Many people overlook the impact of taxes, incorrectly assuming that tax rates will be lower then. While we don’t know for sure what income tax rates will be during retirement, we can consider the impact they have. Take a look:

Therefore, it is important to offset and manage taxes or avoid them altogether. It’s important to note that accessing certain assets may, in fact, raise your tax bracket so it is important to take this into account when planning as well.

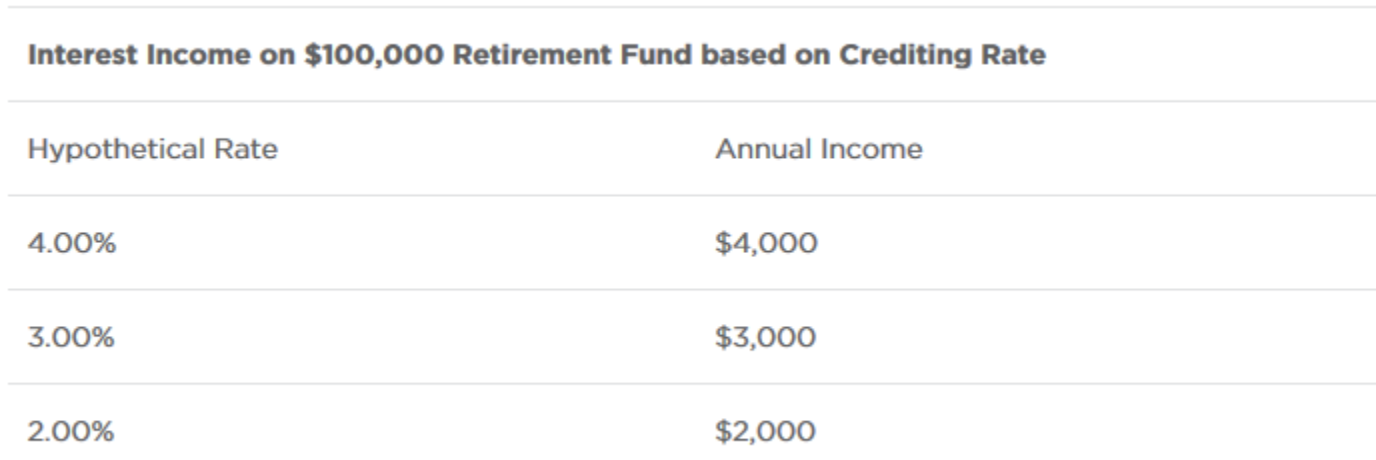

Low Interest Rates. Finally, consider that low interest rates could make some of the sources of your retirement income anemic. The amount of interest a client earns on retirement funds will have a direct impact on the amount available to support his or her lifestyle. Consider that $100,000 will generate the following gross income based on hypothetical interest crediting rates, and depending on the asset, may be income taxable:

What to do?

FlahCo asks the following questions when discussing retirement with clients and co-professional advisors:

What are my chances of becoming chronically or terminally ill?

How can I prevent a long life from becoming a financial burden?

How will I cover gaps in income when interest rates are low?

How do I address the impact on my principal when the market dips?

How will I address the impact of taxes on my income?

Cash value life insurance in its versatility, offers a flexible solution that addresses the 5 roadblocks once qualified plan contributions have been maximized.

Like Term insurance, Cash value life insurance provides a death benefit to help replace income for surviving family members. That’s where the similarities between the two policies ends. And, if designed and funded properly, the cash values can provide a flexible source of tax-free supplemental income in retirement-- with no penalties for distributions made prior to age 59 1/2, unlike qualified plans or IRA money. And the available cash values of a life insurance policy can be used however the client chooses. Accessing money tax-free from a life insurance policy preserves funds from other financial vehicles; this is crucial in down markets. This is why FlahCo clients say cash value life insurance provides tax efficient planning pliancy.

The cash values of a permanent life insurance policy:

Can be accessed on a tax-free basis when withdrawals are structured properly. That is, withdrawals can be taken tax-free up to the cost basis in the policy. Thereafter, policy loans, which are tax-free, can be taken. Note that a policy with loans must be monitored for performance in order to address the loans effect on the policy over time and to avoid an unexpected lapse of the policy.

Can be used as a source of tax-free retirement income during times of market dips to preserve other sources of retirement income.

Can be used to offset taxes that need to be paid on taxable income from other sources

Can be used to offset out-of-pocket healthcare costs like insurance deductibles and co-insurance

Can help to maximize Social Security income by creating the bridge of income required when delaying Social Security benefits to age 70 in order to increase the amount of annual Social Security income.

Can help to lower Medicare Part B premiums since distributions from cash value life insurance are non-reportable for purposes of calculating Medicare Part B premium, which can be as high as $460/month currently.

Moreover, the cash value life insurance policy may include living benefits in the form of riders, such as:

A chronic illness rider which accelerates the death benefit to cover expenses incurred due to chronic illness.

A critical illness rider that provides a one-time lump sum to cover expenses connected to a critical illness like cancer or heart disease, for example.

Note that when cash values are used, or the death benefit is accelerated to provide these living benefits, the death benefit will adjust accordingly.

Remember this: Permanent life insurance delivers income protection during the working years, and is then sufficiently flexible to address the 5 roadblocks clients face during the retirement years.

When it comes to planning for your future, the more information, the better. Stay up-to-date on industry news, learn more about getting started with insurance, and get more familiar with your options by reading our blog.

Contact Us

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.