Equal or Equitable: What's Fair When Planning for the Kids - G.R.O.W.T.H.

G.R.O.W.T.H.

January 1, 2019

Equal or Equitable: What’s Fair When Planning for the Kids

Success can bring sizable wealth. With wealth come benefits, as well as headaches-- such as answering the question, What’s a Fair Inheritance?

To answer this question, there are two bigger questions to answer first:

How to transfer hard-to-divide assets, like a business?

How to equalize the estate among heirs?

Life insurance answers both of these questions:

Life insurance provides readily available cash exactly when needed. This will help with hard-to-divide assets.

Life insurance facilitates fairness and creates a floor that locks in a minimum value for heirs regardless of market conditions

What is fairness?

If a client has a successful business and is planning on passing the business to a family member who is already working in the business, the question becomes how to equalize an inheritance for those heirs who are not working in the business. This question is even more daunting when the business comprises a significant portion of the estate. There are two methods to consider:

Divide up the estate value equally: The value transferred to heirs is based on an equal value in dollar or percentage terms, or

Divide up the estate value fairly: The value transferred to heirs is based on dividing the total estate value by the number of heirs, knowing that the heir(s) working in the business will receive the bulk of the value.

In either approach, life insurance is used to provide the cash needed so the business and other hard-to-value assets do not need to be liquidated. The life insurance helps to define what is fair or equal.

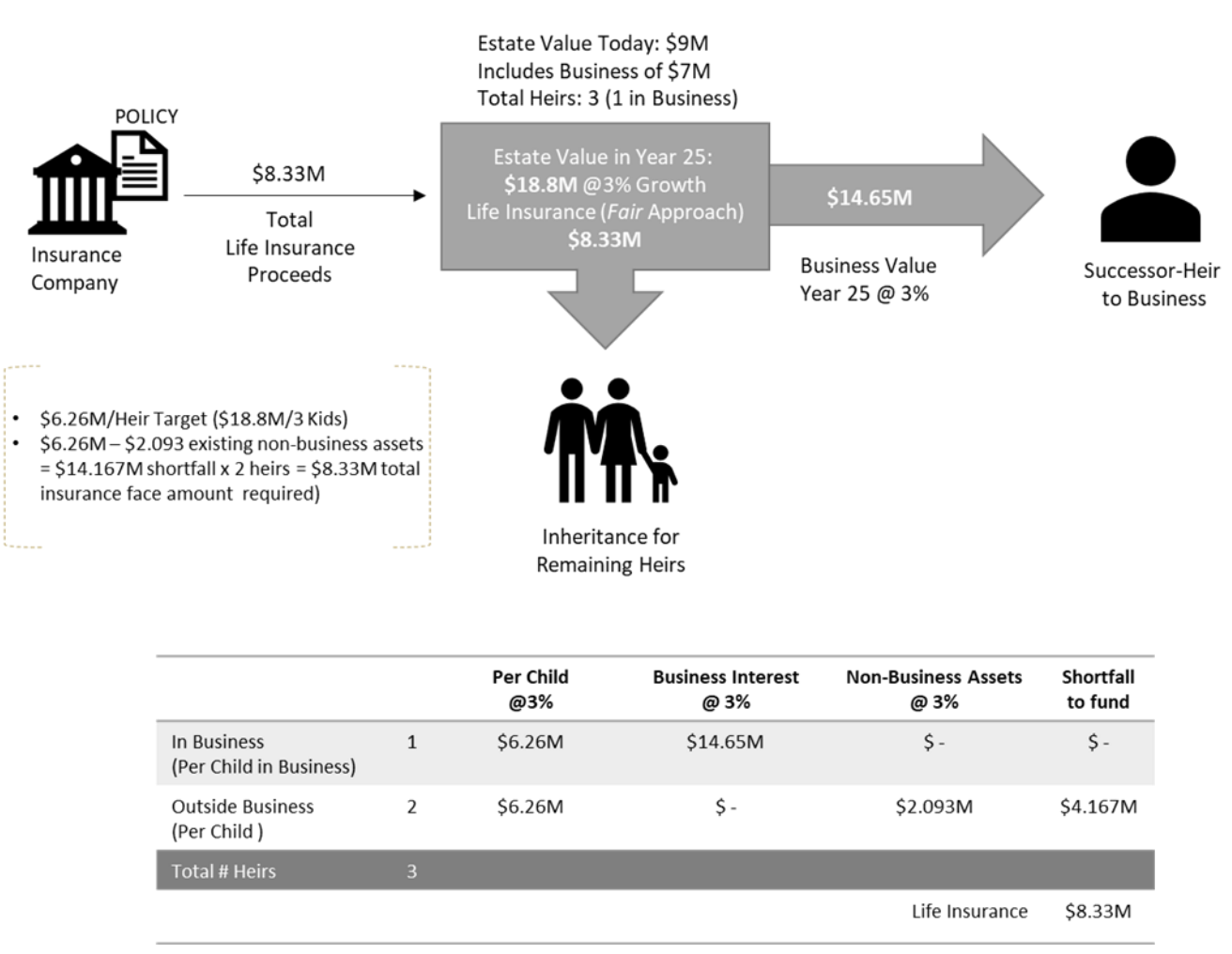

Take this example:

Non-insurance data shown is taken from a hypothetical calculation.

The equal approach requires that the inheritance matches the same dollar amount of the business (or percentage that the business represents of the estate) so that each heir receives a minimum value equal to the business interest. Though this is equal, it may not be feasible to purchase an equal dollar amount of liquidity.

Alternatively, the fair approach, pegs the inheritance to the value of the overall estate and divides that amount by the number of heirs. This way, the inheritance is equitable or fair, even though not equal in dollar value. The child working in the business receives the business (whatever its value) while the other heirs who do not work in the business receive an equal value of estate assets.

Projected Estate Value in Year 25 @ 3% Growth

Benefits of Using Life Insurance to Create a Fair Legacy

Immediate liquidity. The life insurance offers cash exactly when it is needed to facilitate the transfer of a legacy, without having to have heirs sell assets, pay taxes and deplete the legacy in the process. When a family business is being transferred, the cash available helps to keep the business intact so it transfers to the heir(s) without interruption

Minimizes Family Conflict. By planning in advance for the liquidity required to equalize the legacy, heirs receive bequests without conflict, and without costs and the delay of asset liquidation. Heirs are thus more likely to view the legacy as fair.

Creates a legacy Floor. The life insurance policy serves as a “floor” that locks in a minimum value that goes to the family—regardless of the negative impact of a poorly timed market correction or premature death.

Cash Value Life Insurance. Cash value life insurance is particularly suited to the process of equalizing inheritances because it provides income tax-free cash exactly when it is needed—from day one.1 This means that heirs may receive a more favorable return on the premium paid than if those dollars were invested in a taxable investment – that may be subject to market fluctuations. What’s more, the life insurance policy cash values grow tax-deferred and can be withdrawn – up to premiums paid into the contract--on a tax-free basis. Any available distributions above cumulative premiums paid can be taken in the form of tax-free policy loans, if needed. 2

Moreover, when the life insurance policy is owned by a properly drafted trust, the proceeds generally should not be included in your taxable estate.³ A trust is a flexible instrument for wealth transfer, allowing clients to provide detailed instructions for the distribution of estate assets, so that all heirs are treated fairly and equitably – according to the donor’s wishes.

What to Consider

Insurability. Qualification for the life insurance is required in the form of medical and financial underwriting.

Life Insurance Projections. The amount of the death benefit will be affected by the projected growth of the estate so it will be important to carefully consider growth assumptions as they pertain to a client’s particular situation.

Changing Family Dynamics. Consideration of potential future heirs, especially those who may join the business in the future, when planning for a legacy.

Policy & Legal Costs. There are internal costs to the life insurance, as well as legal costs associated with trusts that may be used in the planning. It is important to review planning on a continual basis to ensure that adequacy of the life insurance as needs change, as well as the performance of the policy.

Long Term Care (LTC) or Chronic Illness Benefits (CI). When an LTC/CI rider is included in the policy it is possible to accelerate the death benefit amount during lifetime to cover the costs of long-term care or a chronic illness. When a trust owns the policy, there may be tax consequences to a trust-owned policy when the LTC/CI benefits are exercised. It’s important to work with an advisor who is familiar with such matters.

1 | Life insurance death benefit proceeds are generally excludable from the beneficiary’s gross income for income tax purposes. There are a few exceptions such as when a life insurance policy has been transferred for valuable consideration. No legal, tax or accounting advice can be given by Global Atlantic, its agents, employees or representatives. Prospective purchasers should consult their professional tax advisor for details.

2 | Loans and withdrawals will reduce the death benefit, cash surrender value, and may cause the policy to lapse. Lapse or surrender of a policy with a loan may cause the recognition of taxable income. Policies classified as modified endowment contracts may be subject to tax when a loan or withdrawal is made. A federal tax penalty of 10% may also apply if the loan or withdrawal is taken prior to age 59½. Cash value available for loans and withdrawals may be more or less than premiums paid. It is important to note that when the policy is owned by an Irrevocable Life insurance Trust (ILIT), you will not have access to the policy for loans or withdrawals.

3 | Trusts should be drafted by an attorney familiar with such matters in order to take into account income and estate tax laws (including the generation-skipping transfer tax). Failure to do so could result in adverse tax treatment of trust proceeds.

When it comes to planning for your future, the more information, the better. Stay up-to-date on industry news, learn more about getting started with insurance, and get more familiar with your options by reading our blog.

Contact Us

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.