The coming tax season is a perfect time to help clients assess the options available for their additional savings and to illustrate the flexibility and versatility of cash value life insurance to supplement retirement income.

There are 5 strategic reasons why cash value life insurance can be a powerful savings vehicle for that extra savings objective when compared to other retirement income sources, especially a non- deductible IRA:

Planning for retirement income is a key priority for many pre-retirees between the ages of 40-65.

Social Security and employer- sponsored qualified plans may not provide sufficient income to replace a suitable portion of pre-retirement earnings. Once high-income earners reach their contribution limits to an employer-sponsored plan or an IRA, planning strategically for additional savings becomes critical. Included in the planning process should be an assessment of all available savings vehicles and how the features of each compare to one another relative to:

The question then becomes, which savings vehicles to use? Does a non-deductible IRA make sense? Maybe. Might a cash value life insurance serve as a strategic alternative to a non-deductible IRA? It may.

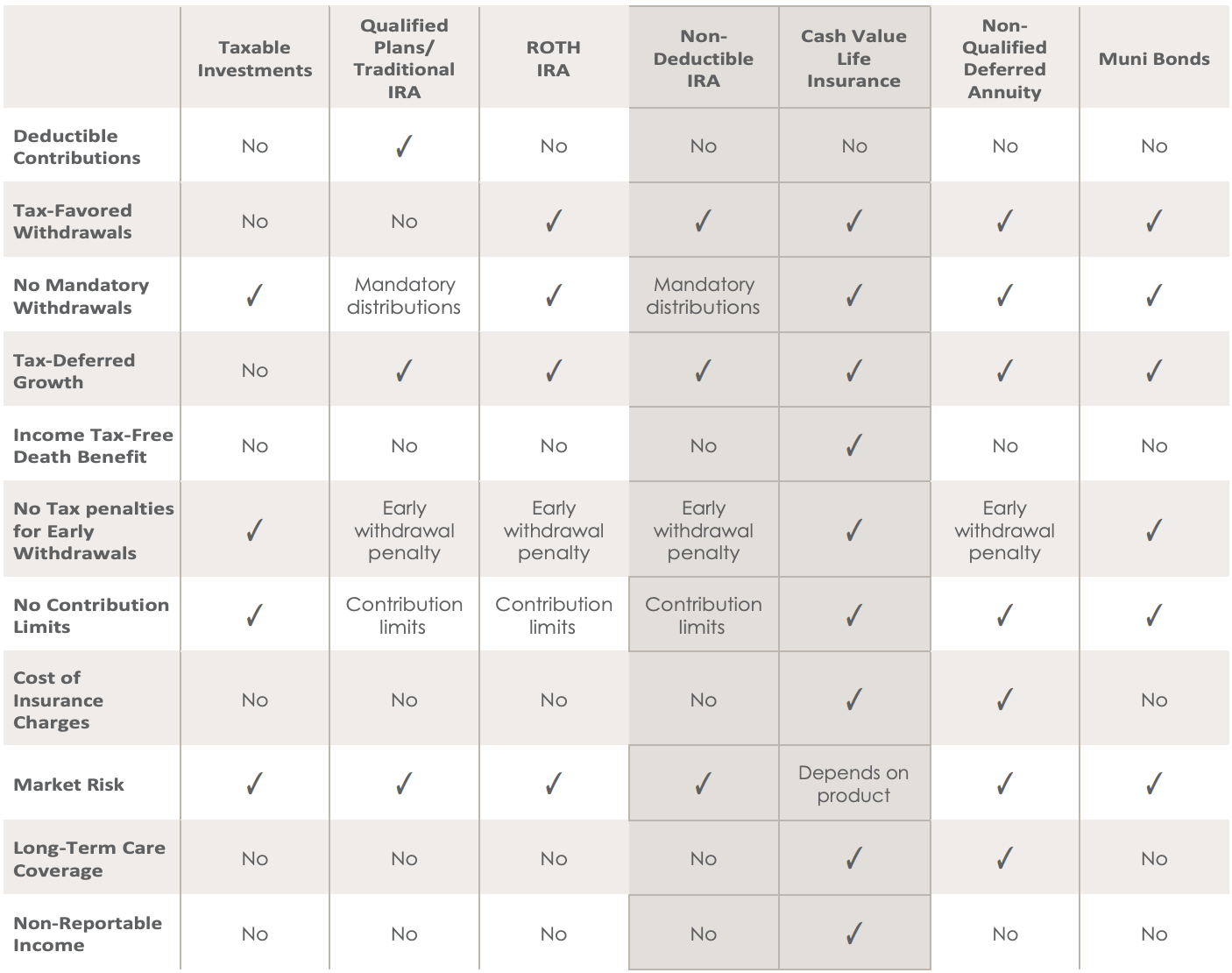

The following comparison chart may help to illustrate why:

Taxable Investments: Capital Gain can be deferred in a taxable investment until shares are sold.

Non-deductible IRAs: Withdrawals from a nondeductible IRA will be pro-rated (partially taxable and partially non-taxable) if there exist other IRAs and/or a gain in the contract. Tax penalty for early withdrawals only applies to taxable amounts from an early withdrawal (pre-59 1/2), and will be pro-rated between taxable and non-taxable amounts of all IRAs owned.

ROTH IRA: Qualified withdrawals from ROTH IRAs are federal income tax free. To be a qualified withdrawal, the withdrawal must occur after the owner 1) has had the ROTH for at least 5 years, and 2) is age 591/2 , is disabled or has died. Some account balances that transfer to a spouse may transfer tax-free. Municipal Bonds: Income from Muni’s may impact SS income and may trigger AMT tax. Tax deferred accumulation in the context of Muni Bonds refers to appreciation.

Life Insurance: Some cash value life insurance products are not tied to the market.