Clients who have informally or formally designated an unneeded IRA as an asset to transfer to the next generation may have heirs who are in for a rude awakening.

Without proper planning, taxes, will deplete the value of the legacy before it reaches the beneficiaries it is intended to support.

When a qualified asset like a traditional IRA or qualified retirement plan is passed to the next generation, the beneficiaries of these assets are required, in many cases, to pay all income taxes on the full amount immediately when received, or over a 5-year period. This is because there is a tax called Income in Respect of a Decedent(IRD) that applies to these types of accounts that have enjoyed tax deferred growth from their pre-tax contributions.

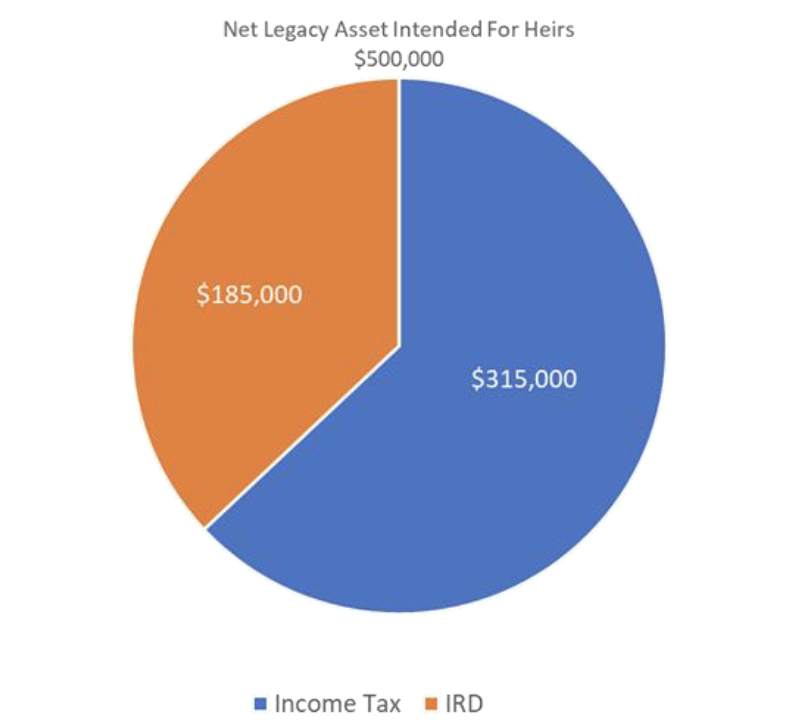

This is a hypothetical example that assumes an IRA value of $500,000 that is intended for heirs is liquidated by the beneficiary when received at the owner’s death as a lump sum and is taxed as such subject to the highest ordinary income tax rate of 37%. There may be other options available to the beneficiary other than a lump sum distribution. This example also does not take into account estate and gift transfer taxes that cab deplete further the net amount passing to heirs. In addition to the negative tax implications of inheriting an IRA or qualified plan asset, is the impact of a market down turn at the time the asset is transferred, as well as the impact on the funds relative to unexpected long-term care expenses. Each of these factors make it challenging to provide a predictable legacy for heirs when transferring a traditional IRA or a qualified retirement plan.

De-risking the legacy with cash value life insurance

By implementing a risk management strategy today that repositions –either a portion of the legacy asset or the income generated from it—into a permanent cash value life insurance policy, clients can minimize the negative impact of taxes, while also building in flexibility to address the negative impact on values due to a market correction or the potential expenses connected to a chronic illness.

Since required minimum distributions must begin at age 70 ½, clients who intend on passing the IRA to heirs must take the distributions anyway, pay taxes and then reinvest in a taxable account. By taking distributions currently, paying taxes and then leveraging those distributions with life insurance, parents can provide a bigger legacy to heirs while also creating a floor beneath which the value of the legacy cannot fall, regardless of market conditions. Moreover, the life insurance provides immediate income tax-free leverage, regardless of when death occurs.

How an IRA Max strategy works:

Now take a look at an example:

Who can benefit from this strategy? Client who:

Are age 59 1/2 or older

Have a minimum new worth of $1,00,00 and sufficient liquid assets

Have an IRA or Qualified Retirement Account that is unneeded for retirement income

Desire to designate an IRA or qualified plan account for heirs

Want to minimize risk to legacy assets from a market down turn and a a chronic illness

Are considering a life insurance policy with a chronic illness or long-term care rider

A cash value life insurance policy can help minimize these risks and maximize funds in 4 ways so the client can live better and leave more:

De-risks the Legacy. The performance of certain cash value life insurance policies is not correlated to the equity, bond or real estate markets. Therefore, the life insurance serves as a “floor” helping to “lock-in” the value of the legacy, offering stability in the form of a predictable amount transferring to heirs—regardless of market conditions.

Converts a portion of a Taxable Legacy into a Non-taxable one. By taking taxable distributions from the IRA or qualified plan to purchase life insurance, the impact of taxes on the legacy are minimized, while creating a larger, non-taxable inheritance.

Offers Tax-advantaged Leverage. The legacy is increased on a tax-favored basis because of the significant leverage the life insurance offers.

Offers Flexibility. It is difficult to plan for every circumstance during retirement. However, life insurance policies that provide living benefits, such as those that allow access to the policy’s death benefit during lifetime to cover costs of a chronic illness or long term care, off flexibility to manage and balance medical expenses with legacy wishes based on changing needs.

When it comes to planning for your future, the more information, the better. Stay up-to-date on industry news, learn more about getting started with insurance, and get more familiar with your options by reading our blog.

Contact Us

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.