The coming tax season is a perfect time to help your high-income clients assess the options available for their additional savings.

There are 5 key reasons why cash value life insurance can be a powerful savings vehicle when compared to other retirement income sources, especially a non-deductible IRA:

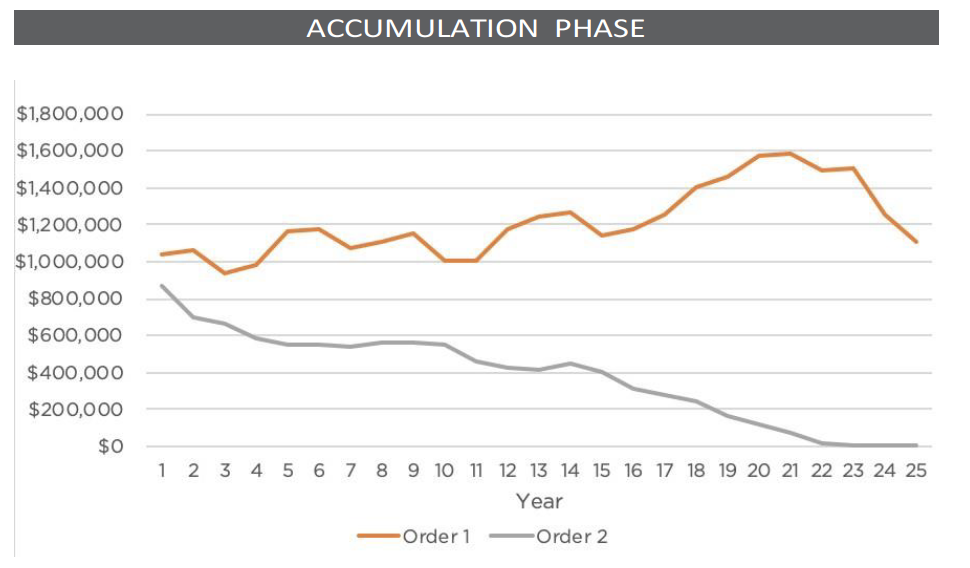

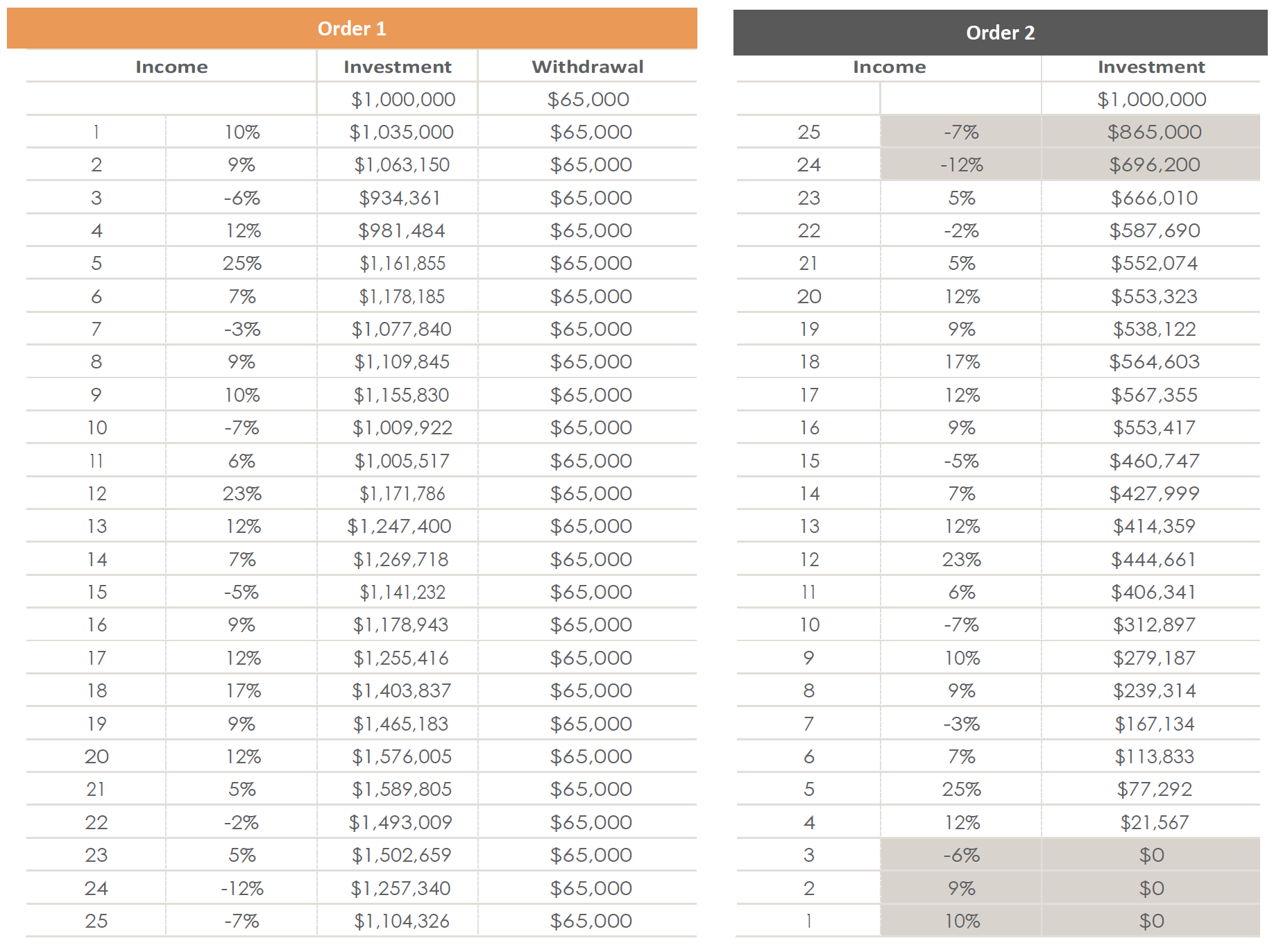

The order of returns doesn’t much matter when accumulating savings. But at retirement, when distributions are taken, the sequence of return really matters. Take a look at a $1,000,000 investment over 25 years. The returns in these two scenarios are exactly the same. The only difference is that they go in reverse direction.

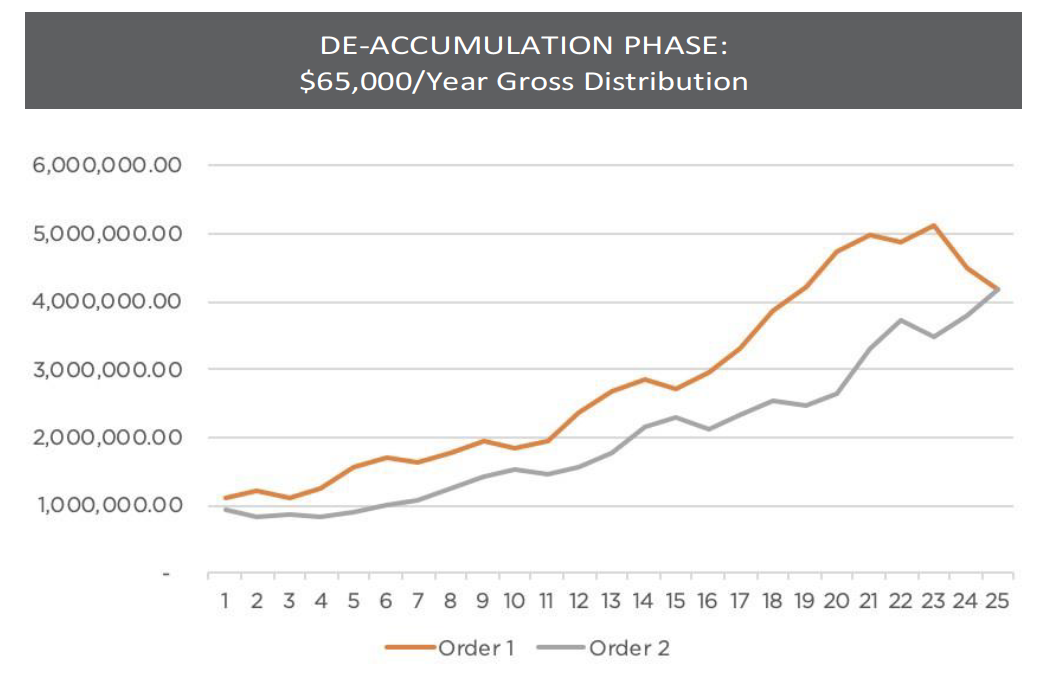

Now look at distributions taken from each scenario:

It’s important to beware of the depletion rate, especially during a market downturn. The withdrawal rates – and not market returns – determine how long retirement funds last. Traditional money management strategies – like asset allocation and diversification – will do little to extend the life of retirement funds during the de-accumulation stage if clients are withdrawing funds too quickly.

Having an alternative source of supplemental income, like cash value life insurance, can help provide a cushion during a market downturn and can go a long way in giving an investment portfolio time to recover. Although some cash value life insurance policies are dependent on market returns, some of these policies have a floor so that while you may not earn interest, your policy may be protected. Other types of policies are not subject to market conditions at all.

How would this work? In a market downturn, instead of taking distributions from a retirement account that has been affected by a “hit” in value, clients can take withdrawals from a strategically designed cash value life insurance policy on a tax-favored basis, while the investment account has time to recover. By considering cash value life insurance for protection needs during the working years, clients will position themselves to have access to a tax-advantaged income source during a market downturn at retirement.

It’s important to consider, too, that the distributions from the life insurance are not considered reportable income. Since Medicare Part B premiums are based on income and can be considerably high (as much as $460/month currently), supplementing income with cash value life insurance may help to keep those premiums down.

Take a look at the following comparison of various options: