The coming tax season is a perfect time to help your high-income clients assess the options available for their additional savings.

There are 5 key reasons why cash value life insurance can be a powerful savings vehicle when compared to other retirement income sources, especially a non-deductible IRA:

During retirement, rising healthcare expenses and the unknown costs of long-term care are some of the main concerns for clients. In addition, because people are living longer – even with chronic illness, clients fear running out of assets. Consider that retirement can last for over 30 years, and that is a good thing1:

Healthcare costs are likely to be the biggest expense throughout retirement. The average out-of-pocket medical costs for a couple age 65 retiring in 2018 is $280,000.2 This figure represents out-of-pocket costs like co-pays, prescription drugs and over the counter costs, not expenses for care associated with a chronic illness or long-term care.

As for long-term care and chronic illnesses, the stats show that one out of every two people will deal with a chronic illness later in life:

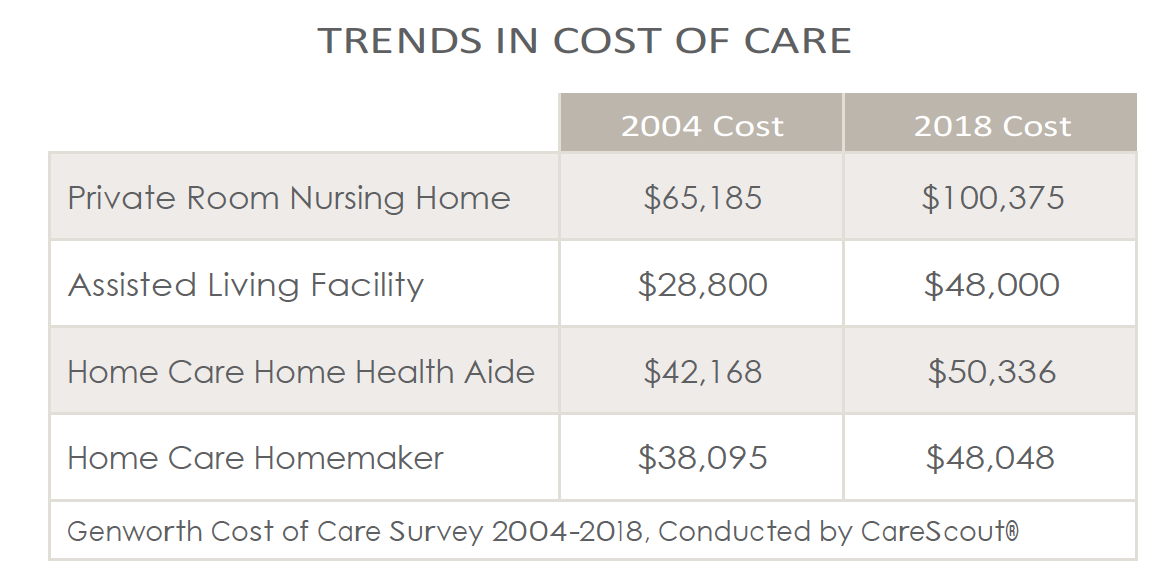

A chronic or terminal illness can cost thousands of dollars each year.

Many clients are concerned about long-term care (LTC) in retirement. There are various sources they may think about to cover these expenses. For example, often clients feel that their health insurance or Social Security will cover LTC costs. That’s not the case. Medicare will cover a very minimal portion of a hospital stay while Medicaid is only available when assets have been completely depleted.

Sometimes clients feel that using savings will be the way out. The problem with this approach is that a surviving spouse may have no funds remaining on which to live. And if there is a market downturn when the funds are needed, that depletes available assets even further. Consider again the chart that compares features of various retirement savings vehicles:

A cash value life insurance policy can preserve retirement assets during an illness or disability. When a long-term care or chronic illness rider is added to the policy, the policy’s death benefit can be used during lifetime to pay for the cost of care, all the while preserving other retirement assets for both spouses in the case of a married couple.

Some insurers offer a critical illness rider that can be added to the policy to secure a tax-free lump sum in the event the insured is diagnosed with cancer, has a stroke or a heart attack, for example. The lump sum payment does not affect the death benefit in most cases and can be used for any purpose including supplementing lost earnings, helping to pay for health care costs not covered by insurance, and providing continued savings or retirement contributions.

Even if these riders are not exercised, the cash value build up in a policy can help with the out-of-pocket medical costs or supplement retirement income. If the policy is never used for any of these purposes, the life insurance proceeds will be available for a surviving spouse’s needs, or as a legacy for heirs. The policy is a flexible and versatile asset in the portfolio that can be used to address changing needs over a lifetime.

1 2015 Valuation Basic Table, Nonsmoker Select and Ultimate mortality rates, Age Last Birthday Basis. American Academy of Actuaries and Society of Actuaries.

2 Health Care Costs for Couples in Retirement Rise to an Estimated $280,000. Fidelity Viewpoints, 4/18/2018. Based on a hypothetical 65-year-old couple retiring in 2018 with average life expectancies that align with Society of Actuaries’ RP-2014 Healthy Annuitant rates with Mortality Improvements Scale MP-2016.