Sometimes strategies can be so simple and basic, yet powerful.

For instance, leveraging the gifts made in the past can go a long way in helping families plan for legacies and the liquidity they will need for their estate planning needs.

That is, an individual who has done planning and has taken advantage of making gifts to a trust in the past has a unique opportunity to leverage those gifts with life insurance, provided medical and financial underwriting is not an issue.

For example, if a client has made gifts in the past to a trust which have now appreciated in value to $5,000,000, a portion of that $5,000,000 can be leveraged with life insurance to increase the value ultimately transferring to the beneficiaries of the trust. This leverage may also be guaranteed so as to diversify assets of the trust and mitigate volatility to the portfolio.

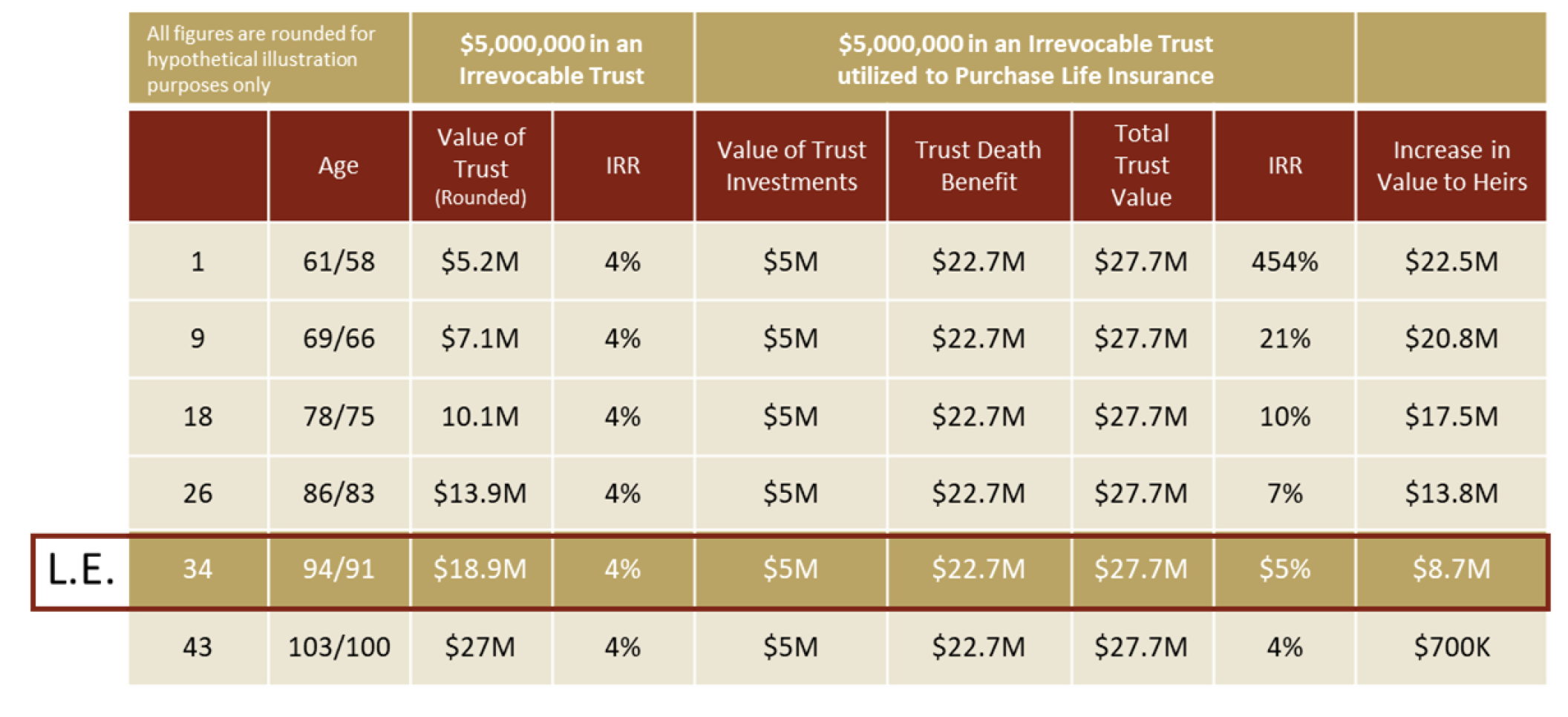

Take a healthy male client, age 60 and female age 57, both non-smokers with preferred underwriting status. Assume they funded a trust years ago and it is now valued at $5,000,000 and earning 4% net after-tax annual income. Also assume the trust allows for the purchase of life insurance.

That annual income (4%) could be repositioned to fund an annual premium of $200,000 that can purchase approximately $22.7 million of life insurance coverage on the couple’s joint lives.

At the couple’s age 94/91 joint life expectancy (L.E.), the trust value—with life insurance-- is $27.7M

With this approach, the client may be able to increase the amount of wealth transferred to the family by $8,728,698 compared to not using insurance.

Take a look:

At joint life expectancy of 94/91, the trust value is approximately $27.7 million. With this approach, the couple can increase the amount of wealth transferred to the family by over $8.7 million.

For clients who have existing trusts and want to potentially increase the wealth that passes to the next generation, they may be able to do so by leveraging existing trust assets.

So simple.